Planning for retirement is a balancing act for physicians who want to retire early enough to enjoy it but also need the financial security to see them through their golden years. That’s why locum tenens is a key element of the retirement strategy for many late-career physicians — it’s a great way to supplement their retirement funds. It can also serve as a smoother transition from full-time work to retirement.

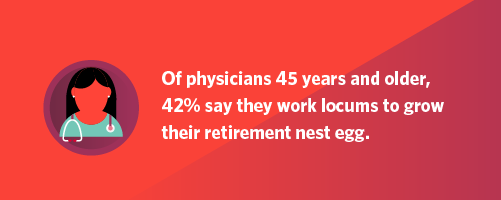

Late-career locum physicians are more likely to use locums work to augment their retirement savings and ease their transition to retirement, according to a 2023 Locum Tenens Experience Survey conducted by Hanover Research for CHG Healthcare. Of physicians 45 years and older, 42% say they work locums to grow their retirement nest egg.

Diverse approaches to locums and retirement

There are many ways physicians use locum tenens to help with retirement, including:

Full-time locums: Emergency medicine physician Dr. Jim Mock works locum tenens full time, which also gave him the flexibility to scale back when he faced a significant health challenge.

Dr. Mock points out that working locums full-time means funding your retirement on your own. “Some companies will match your funding into your pension plan, and that’s an excellent benefit when you work for them, but generally, those companies will pay you much less,” he says.

One of the things he likes best about locums is the ability to be responsible for his retirement plan. “Whatever I put in is what I get,” Dr. Mock says. “If you structure it properly and you’re a good investment guy, you could put away $40,000 a year if you want to.”

Supplemental locums: Psychiatrist Dr. John Hennessee does locums part-time to supplement and diversify his retirement funds. He established a corporate entity — a C Corp — to maximize his retirement contributions and tax savings.

“Any money I earn as a locum really gets paid to the C Corp, and then from there, the C Corp has some paper holdings and holdings of other investments,” he says.

Dr. Hennessee also puts cash investments into IRAs and invests in real estate. While most of his income derives from his work as a physician, he hopes to eventually rely entirely on passive income.

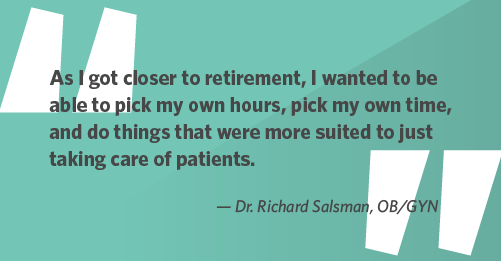

Bridging to retirement: Dr. Richard Salsman, an OB/GYN, uses locums to ease the transition into retirement. “As I got closer to retirement, I wanted to be able to pick my own hours, pick my own time, and do things that were more suited to just taking care of patients,” he says.

Locums has also given Dr. Salsman control over his earnings and savings. “You maximize your retirement plan — you always do that,” he says. Locums “gives you the freedom to work as much as you want, make a lot of money or not make as much money and work less, depending on what you want to do.”

Could it work for you? Why locum tenens makes sense for physicians nearing retirement

Financial planning tips for locums and retirement

Using locums to bolster your retirement stockpile does require some financial planning. Here’s what you need to know.

Structure your locums business

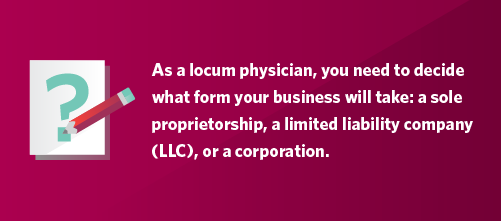

Locum physicians are also business owners. As such, you need to decide what form the business will take: a sole proprietorship, a limited liability company (LLC), or a corporation. Each of these entities comes with unique tax implications.

The simplest option is sole proprietorship. “There’s very little you have to do as a sole proprietor. There’s no entity you need to set up,” explains Chris Hansen, CEO of Personal Choice Financial. However, he notes that sole proprietors must establish separate bookkeeping and bank accounts for their business and personal finances.

LLCs offer “all the simplicity that comes with being a sole proprietor,” Hansen says. However, LLCs limit your business liability outside of malpractice.

With sole proprietorships and LLCs, 100% of your income is subject to self-employment taxes (social security and Medicare payments). C Corporations can reduce that tax burden by dividing your income between a reasonable W-2 salary and a distribution. “That distribution is not subject to a self-employment tax. That’s where a lot of people see significant savings,” says Alexis Gallati of Cerebral Tax Advisors. C Corps also unlock additional tax deductions.

Despite those benefits, C Corps are not for everyone. “It’s extremely complicated,” Hansen says. “You have to have a board. You have to have annual meetings. You have to have an operating agreement. You’re going to spend a lot on legal fees to get it set up and registered properly.”

Continue caring for patients: 4 ways to keep practicing medicine after retirement age

Grow your retirement funds with locums

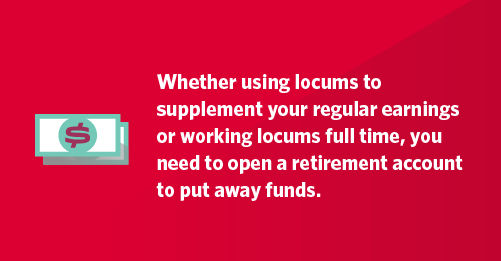

Whether using locums to supplement your regular earnings or working locums full time, you need to open a retirement account to put away funds.

When choosing a retirement plan, “the first question you want to look at is, do I want to save on a pre-tax or a post-tax basis?” says Benjamin Dobler, director of financial planning for Personal Choice Financial.

With a pre-tax 401k plan, you contribute before the earnings are taxed. “You are getting a deduction upfront when you put that money in, and then you pay taxes down the road when you take it out,” Dobler says. “The opposite end of that would be a Roth [IRA], or post-tax contribution.”

He says the option that will work best for you depends on your situation and whether you anticipate your tax rates will be higher or lower when you retire.

Solo 401k plans are inexpensive to administer and allow annual contributions of up to $69,000 for 2024. If you’re over 50, that limit rises to $76,500.

Gallati says another option is to use a defined pension plan with 401k profit sharing. “This is great because, depending on your age, you can put away a ton of money.” She notes that this can be an expensive “administrative hassle,” but most of the time, “the tax benefits outweigh the hassle, in my opinion.”

You can fund a Roth IRA and your 401k to save even more. For high earners, this requires a “backdoor” mechanism, where you make the maximum $7,000 contribution to a traditional IRA, then roll it over to your Roth IRA, Gallati explains.

Saving for retirement can be daunting, particularly the closer you get to retiring. With smart planning, locums can be a valuable component of your late-career physician retirement strategy.

Interested in learning more about locum tenens opportunities? Give us a call at 954.343.3050 or view today’s locum tenens job opportunities.